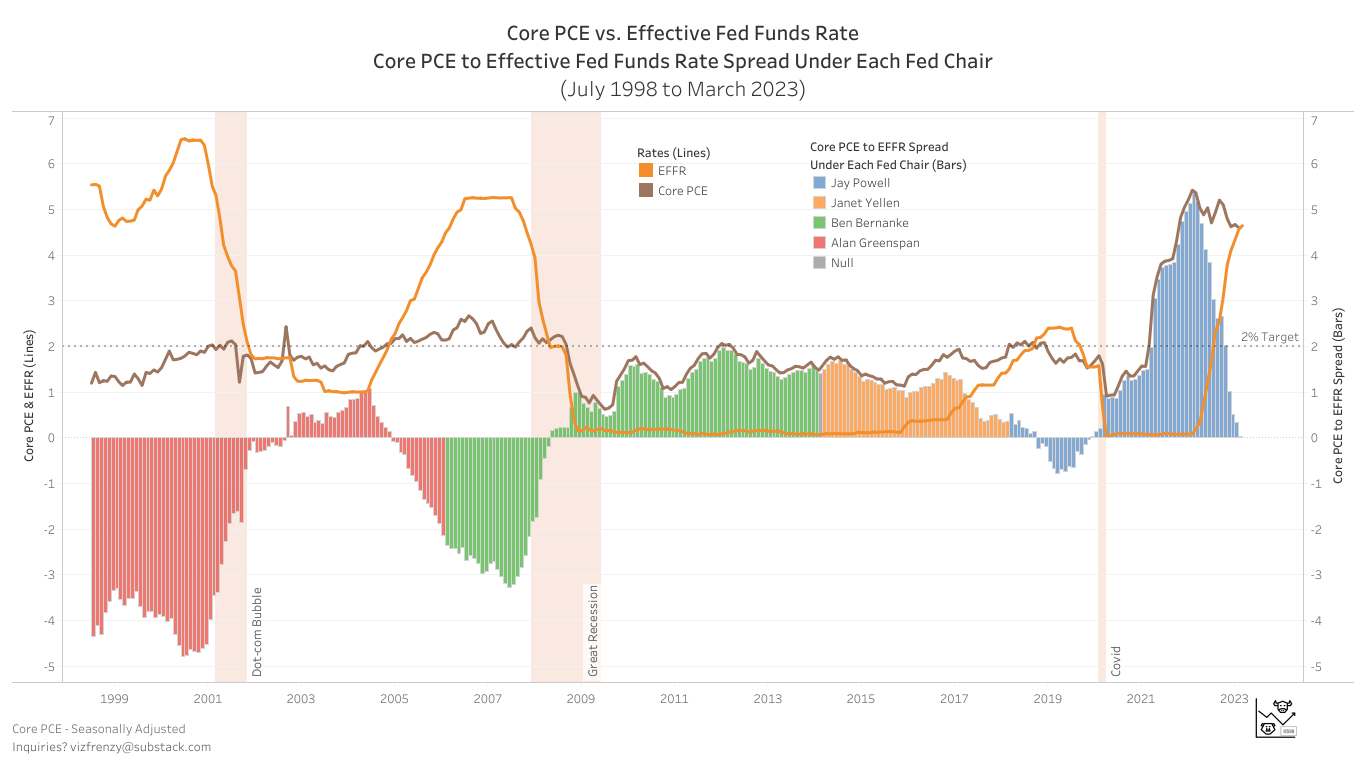

Fed Funds Rate Finally Surpasses Fed's Preferred Inflation Measure

Core PCE Exceeds Federal Funds Rate After 9 Straight Hikes

After nine consecutive hikes, the Federal Reserve has finally raised the federal funds rate above its preferred measure of inflation, core personal consumption expenditures (PCE). Core PCE is a measure of inflation that strips out volatile food and energy prices and is considered a more reliable indicator of underlying inflation trends. The Fed has a target of 2% for core PCE inflation and has been trying to achieve that target since the inflation started in early 2021.

Core PCE vs. Effective Fed Funds Rate - Zoom

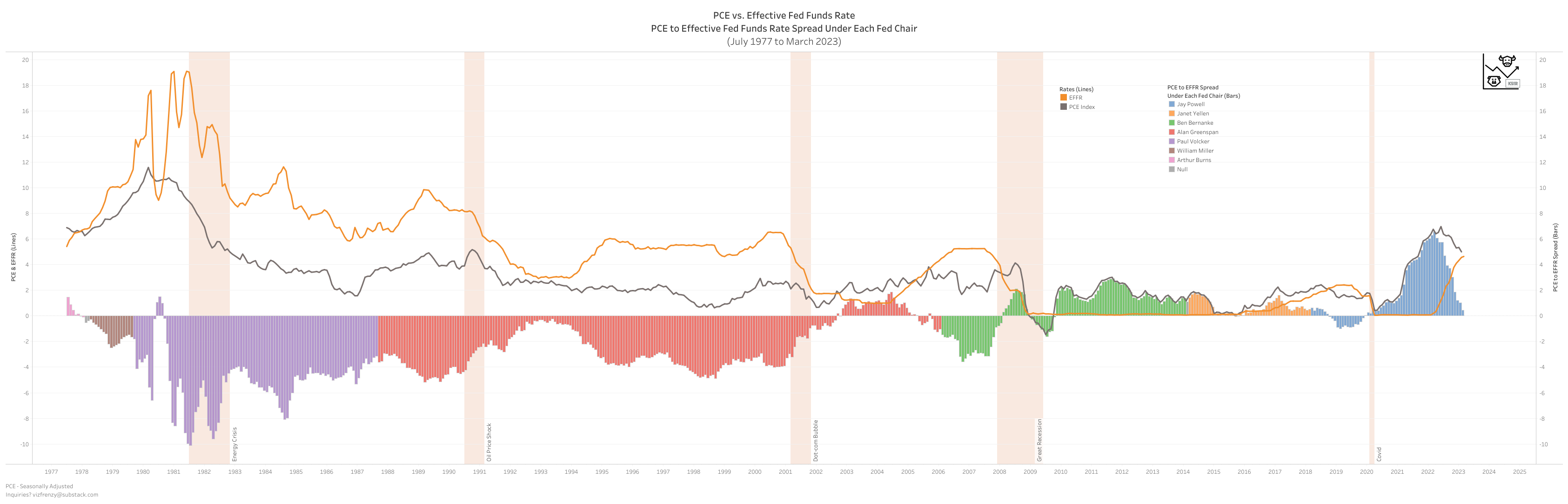

PCE vs. Effective Fed Funds Rate - Zoom

PCE vs. Effective Fed Funds Rate - All

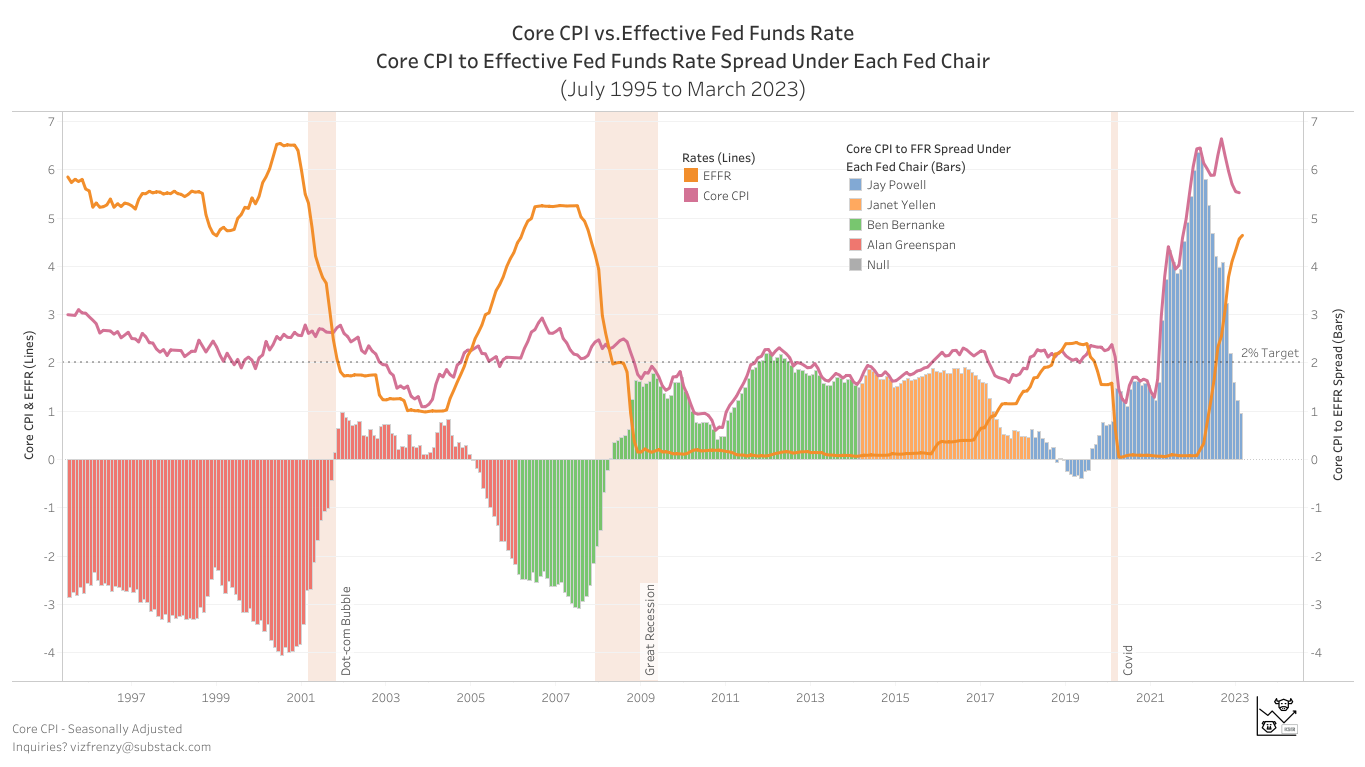

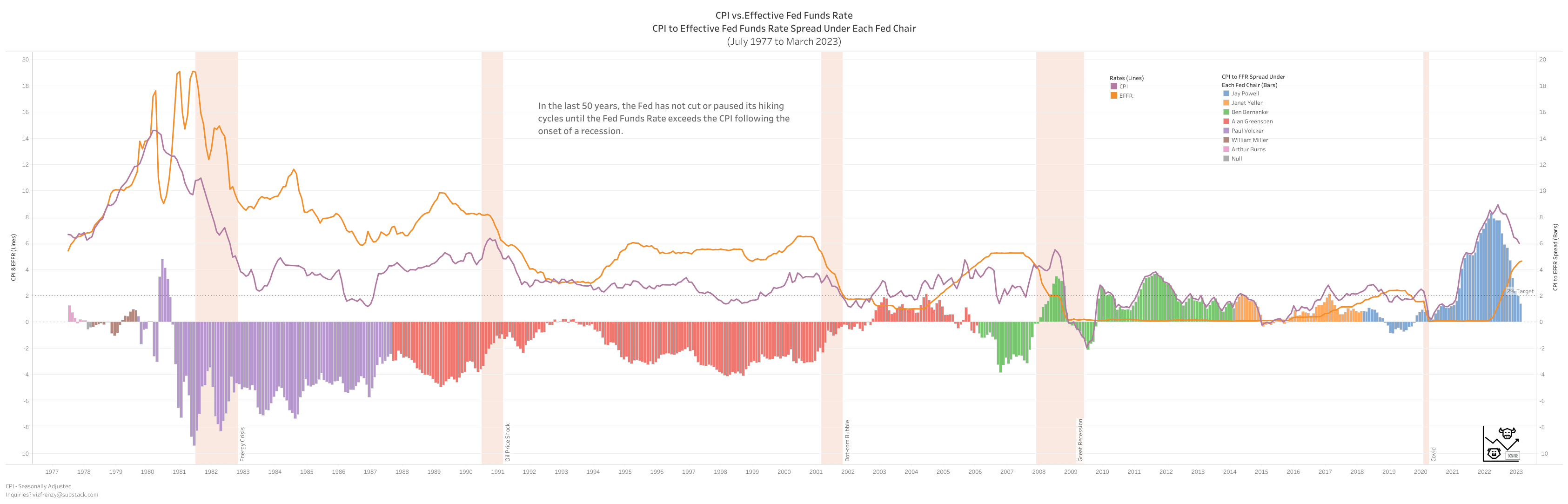

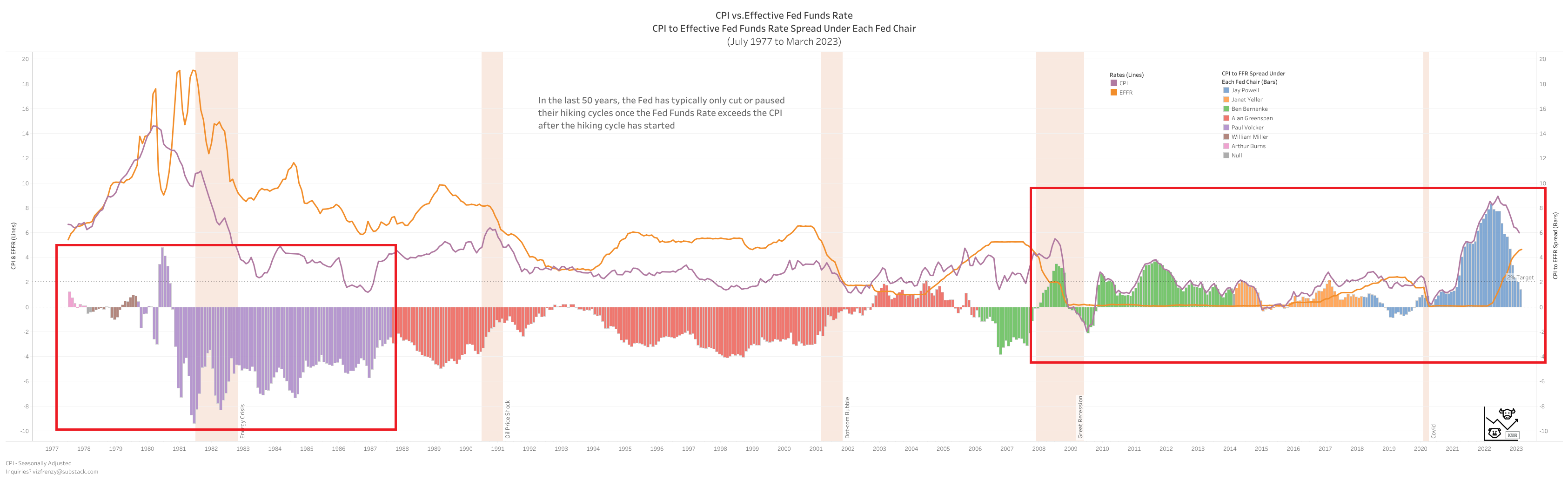

Despite recent increases in the Fed Funds Rate, inflation as measured by the Consumer Price Index (CPI) remains higher than the current rate. In the last 50 years, the Federal Reserve has typically only cut or paused their hiking cycles once the Fed Funds Rate exceeds the CPI after the hiking cycle has started. While it's important to remember that the past cannot predict future outcomes with certainty, it does suggest that the Fed may not need to cut rates unless a significant crisis emerges. The persistently high inflation is due to several factors, including many businesses including utilities are still raising prices. Additionally, there are unforeseen factors contributing to the stickiness of inflation, such as an 8.7% increase in Social Security benefits and Supplemental Security Income (SSI) payments in 2023, and people earning more interest from their savings and money market funds.

Core CPI vs. Effective Fed Funds Rate - Zoom

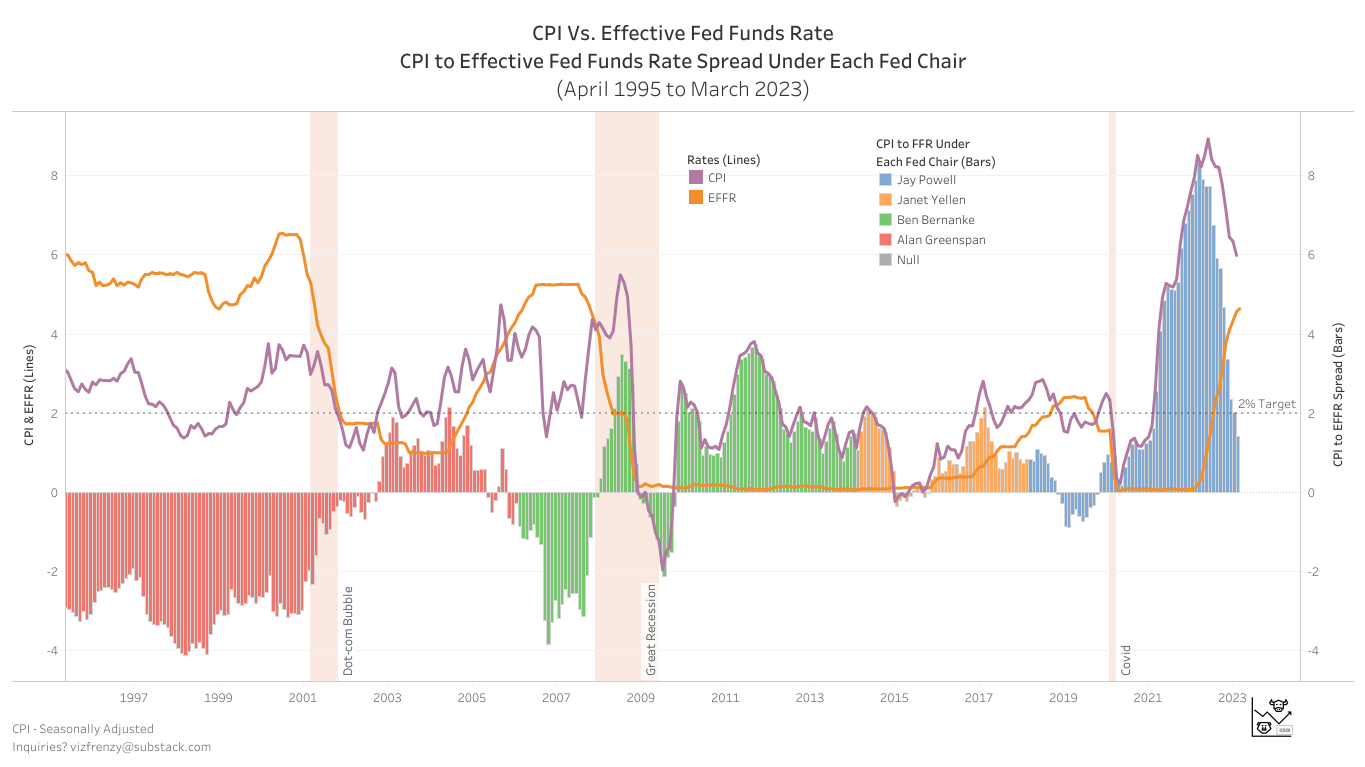

CPI vs. Effective Fed Funds Rate - Zoom

CPI vs. Effective Fed Funds Rate - All

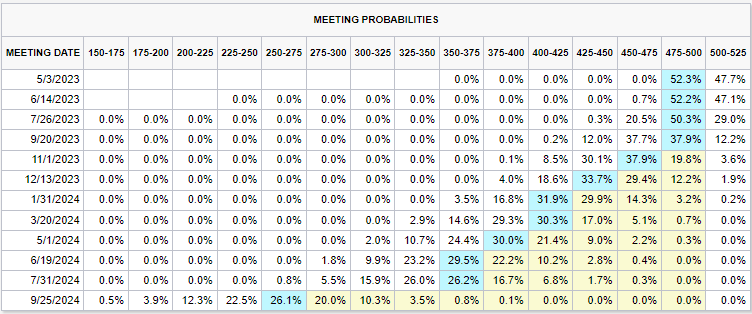

The market's current prediction of a pause in rate hikes and two 25bps cuts by the end of 2023, as reflected in the Fedwatch tool, represents a dramatic shift from just a few weeks ago when the bond market was anticipating a 50bps hike and a terminal rate of over 6%. This change in sentiment can be attributed in part to the recent crisis at Silicon Valley Bank, which has raised concerns about the potential for contagion in the financial sector and increased the perceived risks to economic growth and stability. Additionally, the Federal Reserve has signaled that it believes that the tightening of bank lending standards will also help to replace the necessity of rate hikes previously anticipated. The bond market now appears to be more cautious in its outlook, anticipating that the Federal Reserve will take a more accommodative stance towards monetary policy in response to these uncertainties.

The inflation during the Paul Volcker era is often cited as the worst in US history, with double-digit rates that caused economic instability and reduced purchasing power. However, one aspect that is often overlooked is the real inflation. During that period, the spread between the Consumer Price Index (CPI) and the Federal Funds Rate was actually negative for most months, meaning if you put money in the bank, you get more interest payments than the actual inflation.

In contrast, since the first round of Quantitative Easing (QE) 15 years ago, real inflation has been positive for much of that time. Looking at the bars representing the spread between the CPI and the Fed Funds Rate, it becomes clear that inflation in our world today is even worse in real terms than during the Volcker era.

There are many possible outcomes depending on how things play out in the coming months. It seems clear that we are nearing the end of a hiking cycle, but I'm not very confident that an immediate rate cut is likely. If the Fed does cut rates due to negative economic developments, it may not provide the soft landing that many hope for.